You come back from a three-day industry conference with a folder full of receipts — a $1,200 registration fee, two flights, four nights at a hotel, a handful of meal tabs, and a box of branded brochures you handed out at your booth. You open QuickBooks or Xero, ready to log everything, and the software asks you to pick an expense category. Just one. That moment of hesitation is exactly where bookkeeping mistakes get made, and where IRS compliance quietly starts to slip.

Here is the direct answer: conference expenses do not belong to a single category. Registration fees and course materials fall under Professional Development or Education and Training. Flights, lodging, and ground transportation belong in Travel and Entertainment (T&E). If you were exhibiting, running a booth, or sponsoring a session, those costs are Marketing and Advertising. The IRS requires that every expense be ordinary and necessary for your trade or business under the standard set out in IRS Publication 535 — and the smartest way to stay compliant is to split your conference costs by type from the moment you start logging receipts, not at tax time.

That split sounds simple enough, but the details get complicated fast. The Tax Cuts and Jobs Act (TCJA) eliminated unreimbursed employee expenses as miscellaneous itemized deductions, which changed how employees and employers handle conference costs entirely differently than they did before 2018. Mixed business-and-personal trips trigger the Primary Purpose Test. Meals are still only 50% deductible in most cases. Virtual conferences have their own wrinkles. And if your company reimburses employees for conference travel, you need an Accountable Plan in place or those reimbursements become taxable income.

This guide covers all of it — every cost type, the correct category for each, what changed under TCJA, how to allocate expenses when a conference trip includes personal days, and how to build a clear internal policy so categorization decisions never fall to guesswork again.

Quick Answer: What Expense Category Is a Conference?

A conference is most commonly categorized as a Professional Development or Education and Training expense. That’s the short answer. But the full picture depends on why you’re attending, what you’re paying for, and whether you’re self-employed or a W-2 employee.

Here’s how it typically breaks down:

- Registration fees → Professional Development or Education and Training

- Travel to and from the event → Travel and Entertainment (T&E)

- Hotel and meals → Travel and Entertainment (T&E), subject to the 50% meal deduction limit

- Booth or sponsorship costs → Marketing and Advertising

- Materials, books, or courses bundled with the event → Education and Training

The IRS doesn’t hand you a single box to check. Conference costs tend to spread across two or three categories depending on what the charge actually covers.

The “Ordinary and Necessary” Rule Applies to Everything

Before any category matters, the expense has to pass the baseline test from IRS Publication 535: it must be an ordinary and necessary business expense. Ordinary means common in your field. Necessary means helpful and appropriate for your business. A cybersecurity consultant attending DEF CON? Clear pass. A restaurant owner attending the same conference? Harder to justify.

Self-Employed vs. W-2 Employee — A Critical Distinction

Self-employed individuals and business owners report conference costs on Schedule C, directly offsetting business income. That’s straightforward.

W-2 employees have it worse. The Tax Cuts and Jobs Act (TCJA), which took effect in 2018, eliminated unreimbursed employee expenses as miscellaneous itemized deductions. Gone. If your employer doesn’t reimburse you through an Accountable Plan, you’re likely eating that conference cost with no federal tax benefit at all. Form 2106 still exists but now applies only to specific groups — Armed Forces reservists, qualified performing artists, fee-basis state officials, and employees with disabilities claiming impairment-related work expenses.

When It Crosses Into Multiple Categories

A trade show where you’re also running a booth splits cleanly: registration and travel go under T&E or Professional Development, booth construction and promotional materials go under Marketing and Advertising. Same event, two expense categories. This is cost allocation in practice, and it matters for accurate books whether you’re using QuickBooks, Xero, or FreshBooks.

Virtual conferences follow the same category logic — registration fees still land under Professional Development or Education and Training. You just don’t have the travel line item.

The bottom line: conference registration = Professional Development. Everything else gets sorted by what the charge actually is.

Why It Is Wrong to Put All Conference Expenses Into a Single Category

Most people pick one category — usually “Travel” or “Professional Development” — dump every conference-related receipt into it, and move on. That feels efficient. It’s actually a problem, and not a small one.

Here’s why it matters: different conference costs follow different tax rules. The deductibility percentages aren’t the same across the board. Meals are capped at 50% under current IRS rules. Registration fees are fully deductible as a business expense. A spouse’s airfare may not be deductible at all. If you throw everything into one bucket, you’re either overclaiming deductions you can’t support or underclaiming ones you’re entitled to. Both outcomes cost you money.

The 50% Meal Trap

This is the most common place people get it wrong. When you attend a conference and pay for meals — whether that’s a networking dinner, a lunch between sessions, or a meal you expense during travel days — those costs are subject to the 50% limitation under IRC Section 274. That rule didn’t change with the Tax Cuts and Jobs Act. The temporary 100% restaurant deduction from the COVID-era relief expired after 2022. You’re back to 50%.

If your meals are lumped inside a single “Conference Expenses” line in QuickBooks or Xero, your accountant has no way of knowing to apply the 50% haircut. The software won’t flag it automatically. You have to separate it.

Registration Fees Are Different

Conference registration fees sit cleanly in Professional Development or Education and Training. They’re ordinary and necessary business expenses under IRS Publication 535. No percentage limitation. No entertainment rules attached. Full deduction, assuming the conference is directly related to your trade or business.

That’s a meaningfully different tax treatment from meals. Mixing them in one account obscures both.

Travel Costs Carry Their Own Rules

Airfare, hotel, and ground transportation have their own logic — particularly if you’re combining the conference with personal days. The Primary Purpose Test determines whether those travel costs are deductible at all. If the trip is primarily for business, you can deduct the full round-trip transportation cost. If it tips personal, you may lose it entirely.

That calculation only works if you’ve kept travel costs separate from everything else. You can’t do the primary-purpose math if the airfare is blended into a generic “Conference” category alongside your registration and your dinners.

Employer Reimbursements Add Another Layer

If you’re an employee and your company reimburses conference expenses through an Accountable Plan, the categorization matters at the company level for reporting purposes. Pre-TCJA, employees could sometimes deduct unreimbursed employee expenses via Form 2106 and miscellaneous itemized deductions. That’s gone. TCJA eliminated those deductions for W-2 employees for tax years 2018 through 2025. So if your employer doesn’t reimburse and you’re a W-2 employee, those costs are simply not deductible — regardless of category.

Self-employed people reporting on Schedule C have more flexibility, but they still need proper cost allocation to survive an audit.

What an Auditor Actually Looks For

If the IRS pulls your return and sees a single large “Conference” line item, the first question is: what’s in there? A lump-sum entry with no sub-categorization is harder to defend than a clean breakdown showing $895 registration (Professional Development), $412 airfare (Travel), $220 hotel (Travel), and $87 meals (Meals — 50% deductible). The second version tells a story. The first one invites questions.

Proper category splits aren’t just about getting the deductions right. They’re about being able to show your work.

Primary Category — Professional Development / Education & Training

Registration fees and workshop costs sit most naturally in either a Professional Development or Education and Training expense category. These two labels get used interchangeably depending on your chart of accounts, your accounting software, and whether you’re a self-employed filer or an employee. The functional difference is minor. What matters is that both categories capture costs tied directly to maintaining or improving skills relevant to your current work.

The IRS backs this up. Under IRS Publication 535, education and training expenses are deductible as ordinary and necessary business expenses when the education maintains or improves skills required in your current trade or business — not when it qualifies you for a new one. That distinction matters more than most people realize when they’re filing.

Registration Fees and Tuition Costs

The conference registration fee is the cleanest cost to categorize. Book it under Professional Development or Education and Training and move on. If you’re self-employed, that deduction flows through Schedule C. If you run a business with employees, it’s a straightforward business expense on your books.

For W-2 employees, things got harder after the Tax Cuts and Jobs Act (TCJA) took effect in 2018. Unreimbursed employee expenses — which used to be deductible as miscellaneous itemized deductions on Form 2106 — were suspended through 2025. That means if your employer doesn’t reimburse your registration fee through an Accountable Plan, you’re likely eating that cost with no federal tax benefit. That’s a real hit, and it’s one reason pushing conference costs through a proper company Accountable Plan matters so much right now.

Some conferences blur the line between registration and tuition. A two-day industry event is registration. A five-day credentialing workshop with CEUs might look more like tuition. The IRS doesn’t care much about the label — it cares about the purpose and whether it’s continuing education tied to your existing profession. Attorneys maintaining bar requirements, CPAs completing required CPE hours, nurses renewing clinical credentials — these are textbook Education and Training deductions. Log the credential requirement alongside the receipt if you ever get questions.

In QuickBooks, you’d typically map this to an expense account called “Education and Training” or “Professional Development” under your operating expenses. Xero and FreshBooks both let you create custom expense categories — name it whatever matches your existing chart of accounts, just be consistent year over year.

One practical note on conference passes with tiered pricing: if you buy a VIP or premium pass that bundles in meals, networking dinners, or entertainment access, you may need to split that cost. The portion covering educational sessions stays in Professional Development. The portion covering meals or entertainment hits a different category entirely — and the deductibility rules are different. More on that in later sections.

Speaker Fees and Workshop Materials

If you’re attending a conference as a participant, this one is simple. Workbooks, course materials, required textbooks for pre-conference sessions, printed slide decks sold separately — all of it belongs in Professional Development alongside the registration fee. Keep the receipts and note what they were for.

Where this gets more interesting is if you’re paying speaker fees on the business side — meaning your company hired a speaker for an internal training event or paid for a workshop facilitator. That cost is still Education and Training, but it may also overlap with a business services or contractor expense depending on your chart of accounts. Either works. The key is consistency, and making sure you’ve issued a 1099-NEC if the speaker was paid $600 or more as a non-employee.

Workshop materials specifically tied to a trade show booth or product demo cross into a different category — Marketing and Advertising, not Professional Development. A workbook you take home to improve your own skills? Professional Development. A brochure you hand to prospects at the conference? Marketing. The physical item looks similar. The purpose determines the category.

IRS Publication 463 touches on this in the context of education expenses during business travel, and the Primary Purpose Test becomes relevant when a conference involves both education and business development activity. If you’re attending sessions to learn, that’s Professional Development. If you’re there primarily to meet clients and generate revenue, some of those same costs may shift toward Travel and Entertainment or Marketing instead. You’ll often need cost allocation to split a single conference accurately across multiple categories.

Secondary Category — Travel & Entertainment (T&E)

Once you’ve separated out the registration fee and course materials into Professional Development, you’re left with a pile of receipts that belong somewhere else. Transportation, lodging, and meals all fall under Travel & Entertainment — the T&E bucket — and each one comes with its own IRS rules, deduction limits, and documentation requirements. Get these wrong, and you’re either leaving money on the table or claiming deductions you can’t defend in an audit.

Airfare, Train, and Ground Transportation

Transportation to and from the conference is 100% deductible — but only if the trip is primarily for business. That’s the Primary Purpose Test, and it matters a lot here. If you fly to Chicago for a three-day conference and stay two extra days to visit family, you can’t just deduct the whole ticket. You need to look at how many days were business versus personal. If business days dominate, the round-trip airfare is still fully deductible. If not, you’re allocating costs, and the personal portion comes out of your own pocket.

IRS Publication 463 covers this in detail, and it’s worth reading the transportation section specifically before you file.

What counts as transportation in T&E:

- Airfare and train tickets — economy or business class, the actual cost you paid

- Taxis, rideshares, and car rentals at the destination — getting from the airport to the hotel, hotel to the convention center, etc.

- Parking and tolls — these are deductible on top of the standard mileage rate if you drove your own car

- Baggage fees — yes, these count

If you drove, you can deduct actual vehicle costs or use the IRS standard mileage rate (67 cents per mile for 2024). Track your miles from home to the airport, or from your home or office to the conference location if you drove the whole way.

In QuickBooks or Xero, transportation costs typically go into a “Travel” account within T&E. FreshBooks users will find a default “Travel Expenses” category that works fine. The key is keeping transportation separate from lodging and meals — don’t lump them together into a generic “conference trip” line item.

Hotel and Lodging

Hotel costs are deductible on the nights that serve a direct business purpose. If the conference runs Monday through Wednesday and you arrive Sunday night to avoid an expensive early flight, that Sunday night hotel is still deductible — it’s reasonably necessary. But Thursday night, when the conference is over and you’re sightseeing? That’s personal.

The deduction is 100% for lodging. Unlike meals, there’s no 50% haircut here.

You have two ways to handle this: deduct actual hotel costs, or use GSA per diem rates. The GSA publishes location-specific lodging per diem rates for every city. For expensive destinations like San Francisco or New York, per diem rates can actually be lower than actual hotel costs, so check both before deciding. For cheaper locations, per diem might work in your favor if you found a deal.

Per diem is cleaner from a recordkeeping standpoint, especially for small businesses running under an Accountable Plan for employee reimbursements. Employees submit a per diem claim, the company pays it, no individual receipts required for lodging — though you still need to document the business purpose and dates.

One thing that catches people: hotel incidentals. The minibar charge, the pay-per-view movie, the spa visit — none of that is deductible. Business calls from your room and hotel-provided Wi-Fi are deductible. Pull an itemized receipt when you check out, not just the summary folio, so you can separate deductible from non-deductible charges before you enter anything in your accounting software.

Meals During the Conference

Meals are deductible at 50%. That’s been the rule since the Tax Cuts and Jobs Act (TCJA) locked it in for most business meals starting in 2018. There was a brief window in 2021–2022 where restaurant meals were temporarily 100% deductible to support the industry post-COVID, but that’s gone. You’re back to 50%.

What qualifies: meals you eat while traveling to the conference, meals during the conference days, and business meals with clients or colleagues where there’s a genuine business discussion. That last one still needs the pre-TCJA documentation — who was there, what was discussed, business purpose.

What doesn’t qualify: meals on your personal extension days, alcohol (well, technically deductible but scrutinized heavily), and anything lavish or extravagant by IRS standards — though the IRS has never defined a specific dollar amount for “lavish,” so use common sense.

You can use actual costs or GSA meal per diem rates. GSA breaks meal per diem into three parts: breakfast, lunch, and dinner, with a separate amount for incidentals. If you use per diem for meals, you pick the rate for the conference city, apply 50%, and you’re done. No individual meal receipts required — just documentation that you were there for business.

For employees, how this gets handled depends on whether your company has an Accountable Plan in place. Under an Accountable Plan, the company reimburses the employee, deducts 50% of the meal cost as a business expense, and nothing shows up on the employee’s W-2. Without an Accountable Plan, it gets messy — reimbursements become taxable income, and the employee can no longer deduct unreimbursed employee expenses on Schedule A since TCJA eliminated that deduction for tax years 2018 through 2025. Form 2106 is basically useless for W-2 employees right now unless you’re in one of the narrow exceptions.

Track conference meals separately from other T&E meals in your chart of accounts. Some accountants create a sub-account specifically for “Conference Meals” under T&E to make cost allocation easier at tax time, especially if you’re mixing business and personal days on the same trip.

Correct Categories for Other Common Conference Costs

Not every conference dollar goes under Professional Development or T&E. Some costs belong somewhere else entirely — and misclassifying them can mean losing deductions or creating inconsistencies that flag an audit.

Trade Show and Exhibiting Costs — Marketing & Advertising

If you’re attending a conference as an exhibitor rather than a participant, the primary category shifts. You’re not there to learn. You’re there to generate leads, close deals, or build brand awareness. That makes the bulk of your exhibiting costs Marketing and Advertising, not Professional Development.

This matters because the two categories carry different implications for how you report expenses, how you allocate costs between business units, and how a potential buyer or investor reads your financials. In QuickBooks or Xero, you’d create or use an existing Marketing & Advertising account and code those exhibiting invoices there — not to a training or education account.

The IRS treats ordinary and necessary marketing expenses as fully deductible under IRC Section 162. No 50% meal-and-entertainment haircut. No educational expense limitations. Just a straight business deduction, provided the expense is genuinely promotional in nature.

The line gets blurry when someone from your company also attends sessions at the same conference. In that case, you split: their registration fee goes to Professional Development, the booth costs go to Marketing & Advertising. Clean cost allocation from the start saves headaches at tax time.

Booth Setup, Banners, and Promotional Materials

These are almost always Marketing & Advertising. Full stop.

Booth rental fees, pipe-and-drape charges, electrical hookups, furniture rentals, A/V equipment for your display — all of it is part of the cost of showing up as an exhibitor. Same goes for retractable banners, tablecloths with your logo, brochures, and branded giveaways.

A few practical notes on the specifics:

Booth rental and setup fees — Book these under Marketing & Advertising. If the conference invoices them as a single line item labeled “exhibitor package,” that’s fine. Code the whole thing to marketing.

Printed materials — Brochures, flyers, and data sheets you hand out at the booth are promotional materials. They belong in Marketing & Advertising regardless of whether they were printed specifically for this event or pulled from existing stock.

Branded merchandise and giveaways — Pens, tote bags, USB drives with your logo. These are deductible as advertising expenses under IRS Publication 535 guidelines. There’s a separate consideration for “de minimis” gifts under $4 with your business name on them versus higher-value items that might fall under the $25 gift deduction limit in IRS Publication 463. Keep a record of per-unit cost and total quantity.

Shipping costs — If you shipped booth materials to the venue and back, that freight expense gets allocated to Marketing & Advertising alongside the booth costs. Don’t bury it in a generic “shipping” account if you’re trying to track true marketing spend.

In FreshBooks, you’d tag all of these under the same project or client category so you can pull a complete picture of what that trade show actually cost you.

Sponsorship Fees

Conference sponsorships are a bit of a hybrid, and how you categorize them depends on what you’re actually buying.

If your company pays a fee to get your logo on the conference website, your name announced from the stage, or a banner in the main hall — that’s advertising. Code it to Marketing & Advertising. The IRS treats it as an ordinary and necessary business expense under Section 162, same as a Google ad or a billboard.

If the sponsorship includes a speaking slot or a panel seat for one of your executives, it gets complicated. The speaking opportunity itself has promotional value, but there’s arguably a professional development or thought leadership component too. Most accountants will keep it in Marketing & Advertising since the dominant purpose is visibility and lead generation, not education.

Cause-related sponsorships are different. If you’re sponsoring a nonprofit’s annual conference, part of that fee might be a charitable contribution rather than an advertising expense. You’d need to separate the fair market value of any advertising benefits you receive from the portion that qualifies as a donation — and code them to different accounts accordingly.

One thing to watch: if the sponsorship fee is tied to a table at a conference dinner or gala, you run into the same 50% limitation that applies to meals under post-TCJA rules. Pull that portion out, put it under T&E, and apply the 50% limit. The remaining sponsorship amount stays in Marketing & Advertising at 100%.

Always get an itemized breakdown from the conference organizer when you buy a sponsorship package. It makes cost allocation straightforward and gives you documentation if the IRS ever asks.

How to Categorize Virtual and Online Conference Expenses

Virtual conferences tripped a lot of accountants up during 2020 and 2021, and the confusion hasn’t fully cleared up since. The good news: the categorization logic is actually simpler than for in-person events. The bad news: people still get it wrong by defaulting to old habits.

No Travel Costs, So the Category Splits Differently

With an in-person conference, your expenses spread across Professional Development, Travel & Entertainment, and sometimes Marketing. With a virtual conference, almost everything collapses into one or two buckets.

The registration fee goes under Professional Development / Education & Training. Same as always. The IRS doesn’t care whether you attended in a hotel ballroom or your spare bedroom — if the content qualifies as an ordinary and necessary business expense under IRS Publication 535, the category is the same.

What changes is that the T&E bucket is mostly empty. No flights. No hotel. No per diem calculations. No GSA per diem lookups. That’s a good thing — it removes most of the complexity.

What Costs Actually Exist for Virtual Conferences

Here’s what you’ll realistically be categorizing:

- Registration fee → Professional Development / Education & Training

- Required software or platform access (e.g., a paid Zoom license you didn’t already have, a temporary event platform subscription) → Computer and Software Expenses, or fold into Professional Development if it’s a one-off tied directly to the event

- Home office costs (upgraded bandwidth for the week, a headset you bought specifically for sessions) → these are trickier

That last category is where people make mistakes. Buying a $150 headset to attend a virtual conference isn’t automatically a conference expense. It’s equipment. Put it under Office Equipment or Computer Hardware in QuickBooks or Xero. If you’re on Schedule C, it may qualify for Section 179 expensing depending on business-use percentage.

The Home Office Angle

If you work from a dedicated home office, your regular home office deduction already accounts for a portion of your internet costs. Don’t double-count. The incremental cost of a bandwidth upgrade specifically for a three-day virtual event? That’s defensible as a direct conference expense. Your normal monthly Comcast bill? Not additionally deductible just because you attended a webinar on it.

This matters more than people think when you’re self-employed and filing Schedule C. The IRS has seen enough creative home-office deductions that this is an audit flag area. Keep the logic clean.

Employee Reimbursement for Virtual Conference Costs

If you’re an employer reimbursing staff for virtual conference attendance, the same Accountable Plan rules apply as with any other expense. The employee submits receipts, the reimbursement ties to a legitimate business purpose, and any excess gets treated as wages.

Worth noting for employees: unreimbursed employee expenses for W-2 workers are not deductible at the federal level after the Tax Cuts and Jobs Act (TCJA) eliminated miscellaneous itemized deductions. Form 2106 is essentially useless for most W-2 employees until 2026 at the earliest under current law. So if your employer won’t reimburse your $499 virtual conference registration, that cost is just gone from a federal tax perspective. Some states still allow it — California being the main one — but federally, it’s dead.

How to Record It in Accounting Software

In QuickBooks, create or use the existing Professional Development expense account for the registration fee. If the software purchase is genuinely reusable beyond the conference, put it in a Software Subscriptions account instead. Don’t lump everything under one line item just because the event was online.

FreshBooks users: the category structure is simpler, but the same logic applies. Tag the registration fee separately from any equipment purchases so your year-end reports actually mean something.

The cleaner your cost allocation is throughout the year, the less time you spend reconstructing things in March.

How to Classify Local Conference Expenses When There Is No Travel

Local conferences strip out the travel complexity, but they don’t simplify the categorization question as much as people assume. You still need to split costs correctly. The fact that you drove twenty minutes instead of flew six hours doesn’t change the IRS rules around what each dollar was spent on.

No Travel Doesn’t Mean One Category

When there’s no overnight trip involved, you lose the lodging and airfare line items — but the registration fee, meals, parking, materials, and any sponsor or booth costs still each belong in their own bucket.

Here’s how the core costs typically break down for a local conference:

Registration fee — Professional Development or Education and Training. Same rule as any other conference. The fee covers the educational content, so that’s where it lives.

Parking and mileage — Travel expense, even locally. The IRS treats your car costs as travel regardless of distance. Use the standard mileage rate (67 cents per mile for 2024) or actual costs, and log it separately. Don’t fold it into the registration fee on your books.

Meals at the event — Meals and Entertainment, capped at 50%. The TCJA made this painful but it didn’t go away. A catered lunch included in your registration is a problem area. If the meal cost is bundled into the registration fee and not broken out on the invoice, you have two options: ask the organizer for a breakdown, or use a reasonable estimate and document your methodology. QuickBooks and Xero both let you split a single transaction across categories — use that feature.

Business cards, printed materials, or handouts you bring — Marketing and Advertising. You’re distributing those to generate business, not to educate yourself.

A booth or table at a local trade show conference — Marketing and Advertising, full stop. Booth rental is a promotional cost under Schedule C or your business’s operating expenses, not a training expense.

The “No Overnight Stay” Effect on Deductibility

Here’s where local conferences actually work in your favor. The Primary Purpose Test and the foreign/domestic travel rules under IRS Publication 463 are built around trips with overnight stays. For a local conference you attend and come home from the same day, those tests don’t apply the same way.

That means you don’t need to calculate a business-vs-personal day split. The whole day is a business day if the conference is the reason you went. Simple.

What you do still need: a clear business purpose. “Networking” alone is weak. “Attended the [conference name] annual symposium relevant to my [specific practice/industry] to satisfy continuing education requirements and meet prospective clients” is defensible.

Employees vs. Self-Employed — The Reimbursement Split

If you’re self-employed, local conference costs go directly on Schedule C under the appropriate categories. Straightforward.

If you’re an employee, this gets thornier. Post-TCJA, unreimbursed employee expenses are no longer deductible as miscellaneous itemized deductions for federal purposes. That deduction is gone through 2025 at minimum. So if your employer doesn’t reimburse you, you generally can’t deduct local conference costs on your federal return.

The fix is getting your employer to set up an Accountable Plan. Under an Accountable Plan, your reimbursements aren’t taxable income to you, and your employer deducts them as a business expense. The employee submits receipts, gets reimbursed, and the cost is categorized on the company’s books — not yours. If you’re in HR or manage a small team, pushing for an Accountable Plan structure saves everyone money.

Tracking It in Practice

For a local conference, your expense record should capture:

- Date and name of the conference

- Business purpose (specific, not generic)

- Total registration cost

- Mileage or parking, logged separately

- Any meal costs, split out with the 50% limitation flagged

- Any marketing materials brought or distributed

FreshBooks users can attach a photo of the receipt directly to the expense entry and add a note field — use the note field for the business purpose description. That documentation habit matters if you’re audited. The IRS doesn’t just want the number; they want to see that you knew why you were there.

Mixed Business-Personal Conference Trip — Expense Allocation Rules

Plenty of people tag a few vacation days onto a conference trip. That’s fine. The IRS isn’t going to tell you how to spend your weekend. But how you categorize the costs depends entirely on why you went in the first place — and that determination has to happen before you start splitting anything.

The IRS Primary Purpose Test

The Primary Purpose Test is the IRS’s way of deciding whether your trip was fundamentally a business trip with some personal time mixed in, or a personal vacation that happened to include a conference. It’s not a form you fill out. It’s a judgment call based on facts, and you need to document those facts.

The rule is straightforward. Count the total days of the trip. If more than half of them were spent on legitimate business activity, the trip passes the Primary Purpose Test and the transportation costs — flights, train tickets, mileage — are fully deductible. If personal days outnumber business days, none of the transportation is deductible at all.

That’s a hard line. A 10-day trip where you attended a 4-day conference and spent 6 days sightseeing means zero deduction for your airfare. IRS Publication 463 spells this out clearly.

What counts as a business day? Days you actually attend conference sessions. Travel days to and from the destination. Days you’re unable to work due to circumstances outside your control — a canceled flight, a medical issue. Weekends and holidays sandwiched between business days also count if it would have been unreasonable to travel home and back.

What doesn’t count? The day you decided to stay an extra four days to visit your cousin. A “recovery day” you invented. Any day that was purely personal in nature.

Document everything. Keep the conference agenda. Save your registration confirmation. If you had client meetings or site visits outside the main conference, write up a brief contemporaneous note — date, who you met, what you discussed. The IRS has seen every version of “I was working the whole time,” and documentation is the only thing that actually holds up.

Splitting Costs by Day — Which Days Count as Business and Which Count as Personal

Once you know the trip passes the Primary Purpose Test, transportation is fully deductible and you stop worrying about it. What you still have to split are the daily costs — hotel, meals, per diem, and incidentals.

The split is mechanical. Take the total number of days in the trip. Divide the daily costs by that number to get a per-day figure. Multiply by the number of business days. That’s your deductible portion. The personal-day costs are just personal expenses — they go nowhere on your return.

Say you fly to Chicago for a 3-day conference, then stay 2 extra days for personal reasons. Total trip: 5 days. Hotel runs $200/night, so $1,000 total. Three business days ÷ five total days = 60%. You can deduct $600 of the hotel cost. The $400 for the personal nights? That’s on you.

Meals follow the same logic, but remember the 50% limitation still applies after the allocation. So $150 in deductible business meals becomes $75 after the IRS’s standard meal deduction cap. If you’re using GSA per diem rates instead of actual receipts, apply the same day-count ratio before the 50% haircut.

If you’re running this through an Accountable Plan for employee reimbursements, the same allocation rules apply. You can only reimburse — and deduct as a business expense — the business-day portion. Reimbursing personal days through an Accountable Plan blows the plan’s tax-favored status for that payment, which creates a wages issue.

One practical tip: book your hotel nights separately if you can. Pay for the business nights on your business card and the personal nights on your personal card. It eliminates the allocation math and makes the audit trail obvious. Not always possible, but worth doing when it is.

Track this in QuickBooks, Xero, or FreshBooks by creating a split transaction. Log the full expense, then split the line items — business portion to the appropriate expense account (Travel, Professional Development, or wherever it belongs), personal portion to an owner’s draw or non-deductible account. Don’t just net the personal days out of your head and enter a smaller number. The full amount needs to be on record with the split clearly documented.

Employee vs. Employer — How Conference Expense Treatment Differs

The same conference can be treated completely differently on paper depending on who pays and how. Getting this wrong creates real problems — either missed deductions or reimbursements that get taxed as income when they shouldn’t be.

When the Employer Pays Directly

If the company puts the conference registration on a corporate card, books the flights, and pays the hotel invoice directly, there’s no ambiguity. The business deducts those costs through the appropriate expense categories — registration under Professional Development or Education and Training, travel under Travel & Entertainment, meals at 50%, and so on.

The employee receives no taxable income from any of it. Nothing shows up on their W-2. The employer just needs clean documentation: the business purpose, who attended, and receipts for anything over $75. That’s it.

One thing employers sometimes miss: if a conference ticket is purchased for a client or a prospect, it stops being an Education and Training expense. That’s Marketing and Advertising — or possibly a gift subject to the $25 per-recipient limit. Category matters even when you’re paying directly.

Employee Reimbursement Under an Accountable Plan

An Accountable Plan is the mechanism that lets employers reimburse employees tax-free. It has three requirements under IRS rules: the expense must have a business connection, the employee must substantiate it (amount, date, place, and business purpose), and any excess reimbursement must be returned within a reasonable time.

When all three conditions are met, the reimbursement never touches the employee’s taxable income. The employer deducts it as a business expense. Everyone wins.

The practical side: you need a written Accountable Plan policy. Verbal agreements don’t hold up under audit. The policy should state the submission deadline — most companies use 60 days from when the expense was incurred — and the return deadline for excess advances, typically 120 days.

For conference travel, you can reimburse based on actual receipts or use GSA per diem rates for lodging and meals. Per diem simplifies accounting because you skip collecting individual meal receipts. Just confirm you’re using the correct GSA per diem rate for that city and travel dates, since rates change annually and vary by location.

Reimbursements paid outside an Accountable Plan are called non-accountable plan reimbursements. Those get added to the employee’s W-2 wages, subject to payroll taxes. The employee can’t deduct them either. Avoid this structure entirely if you can.

When the Employee Pays Out of Pocket — Unreimbursed Expenses After TCJA

This is where it gets painful for employees. Before 2018, unreimbursed employee expenses — including conference registration, travel, and related costs — could be deducted as miscellaneous itemized deductions on Schedule A, subject to the 2% of adjusted gross income floor. Annoying, but available.

The Tax Cuts and Jobs Act wiped that out. Starting in 2018 and running through at least 2025, employees cannot deduct unreimbursed work expenses on a federal return. If your employer doesn’t reimburse you for that $1,200 conference and $600 flight, that money is simply gone from a tax perspective.

There’s no Form 2106 workaround for regular W-2 employees anymore. Form 2106 still exists but is now limited to specific groups: Armed Forces reservists, qualified performing artists, fee-basis state and local government officials, and employees with impairment-related work expenses. If you’re a standard salaried employee, you don’t qualify.

Self-employed people are in a different position entirely. If you attend a conference as a sole proprietor or single-member LLC, you deduct qualifying conference expenses on Schedule C as ordinary and necessary business expenses. The TCJA changes to unreimbursed employee expenses don’t affect you — you were never using that deduction in the first place.

The practical takeaway for employees: push for reimbursement. If your company doesn’t have a formal expense reimbursement policy for conference costs, ask for one. An Accountable Plan costs the company nothing extra and saves you from absorbing a significant out-of-pocket hit with zero tax relief.

Conference Tax Rules After the Tax Cuts and Jobs Act (TCJA) — What Changed

The TCJA, signed into law in December 2017, rewrote several rules that directly affect how conference expenses are deducted. Some changes were minor. Others were significant enough that what worked on your 2017 return no longer works today.

The Elimination of Unreimbursed Employee Expense Deductions

This is the big one. Before 2018, employees who paid out-of-pocket for conferences — and weren’t reimbursed by their employer — could deduct those costs as unreimbursed employee expenses on Form 2106. Those deductions flowed into miscellaneous itemized deductions on Schedule A, subject to a 2% of AGI floor. Not ideal, but it existed.

The TCJA eliminated that deduction entirely for tax years 2018 through 2025.

So if you’re a W-2 employee and your company doesn’t reimburse your conference registration, travel, or hotel costs, you currently get zero federal tax benefit from those expenses. None. That’s a real financial hit for employees in fields like healthcare, law, or finance where conferences are genuinely necessary for licensing or professional standing.

The suspension is scheduled to expire after 2025. Whether Congress extends it is a separate question, but as of now, the limitation stands.

What This Means for Employers

The practical consequence is that smart employers set up an Accountable Plan. Under an Accountable Plan that meets IRS requirements, reimbursements for qualifying conference expenses are excluded from the employee’s taxable income — and the employer deducts them as a business expense. Everyone wins.

Without an Accountable Plan, reimbursements can get messy. They may be treated as taxable wages to the employee and the employer’s deduction still holds, but the employee ends up with a tax bill on money they effectively spent on business.

If you run payroll and reimburse employees for conferences, talk to your accountant about whether your current reimbursement policy qualifies as an Accountable Plan. The IRS requirements aren’t complicated, but they do matter.

Self-Employed Individuals — The Rules Are Different

If you’re self-employed — sole proprietor, single-member LLC, partnership — the TCJA didn’t gut your conference deductions. You still deduct ordinary and necessary business expenses on Schedule C or your partnership return. Qualifying conference costs continue to flow through there, subject to the same rules that always applied.

Professional development, registration fees, travel under the Primary Purpose Test, lodging — all still deductible for the self-employed, assuming the expense is ordinary and necessary under IRS Publication 535 standards.

The Meals Deduction — The 50% Rule Still Applies, With a Catch

Meals at conferences were already subject to a 50% deduction limit before the TCJA. That didn’t change.

What the TCJA did affect was entertainment. Before 2018, business entertainment expenses — think client dinners at a conference, hospitality suites, taking a prospect to a game after the tradeshow — were 50% deductible if they met the directly-related or associated-with test. The TCJA repealed that entirely. Business entertainment is now nondeductible. Zero.

The IRS clarified in Notice 2018-76 that meals remain 50% deductible if they’re separately stated from entertainment costs and meet the ordinary and necessary standard. So if you take a client to a conference dinner and the restaurant issues one check, you need to break out the food cost separately to preserve any deduction. If it’s bundled together as “entertainment,” you lose it all.

That distinction matters at conferences where meal functions and networking events blur together. Keep your receipts itemized.

Per Diem Rates After TCJA

The TCJA didn’t change the per diem system itself, but the IRS adjusts GSA per diem rates annually and the numbers do shift. For 2024, the standard per diem rate for most U.S. locations is $166 per day ($107 for lodging, $59 for meals and incidentals). High-cost locations run higher.

Self-employed individuals can use per diem rates for meals but not lodging — they must use actual lodging costs. Employees reimbursed under an Accountable Plan can use per diem for both. That’s been the rule for a while, but it’s worth knowing when you’re estimating conference costs or setting up a reimbursement policy.

The Corporate Entertainment Facility Rules

One niche area that occasionally comes up at large conferences: entertainment facilities. If your company rents out space at a conference venue for a client event — a private dinner, a hosted cocktail reception — that cost used to be partially defensible as a business expense. Post-TCJA, those entertainment-adjacent facility costs face much stricter scrutiny. The IRS views anything that blurs into entertainment with skepticism, and the TCJA gave them the statutory backing to deny it.

Sponsoring a conference booth is marketing. Hosting a cocktail party at that conference? Your accountant should review that carefully before you call it a business deduction.

Through 2025 — and Then What?

Most TCJA individual provisions sunset after December 31, 2025. The reinstatement of miscellaneous itemized deductions — including unreimbursed employee expenses — is theoretically possible if Congress doesn’t act. Whether that happens, and what form it takes, remains uncertain.

If you’re an employee currently eating conference costs out of pocket, it’s worth keeping records now. If the deduction comes back, you’ll want documentation ready. IRS Publication 463 covers the recordkeeping requirements, and those haven’t changed regardless of TCJA.

The IRS Ordinary and Necessary Rule — What Makes a Conference Expense Deductible

Before you categorize anything, you need to clear the first hurdle: does the expense actually qualify as deductible? The IRS doesn’t care how you label a cost in QuickBooks if the underlying expense can’t pass a basic two-part test.

That test comes from IRC Section 162. An expense must be both ordinary and necessary to your trade or business. That’s it. Two words, but they do a lot of work.

What “Ordinary” Actually Means

Ordinary doesn’t mean you spend money on it every day. It means the expense is common and accepted in your industry. Attending an annual medical conference is ordinary for a physician. Attending the same conference as a freelance copywriter writing a blog post about healthcare? Probably not.

The IRS looks at what’s normal for your specific business, not businesses in general. So context matters enormously here.

What “Necessary” Actually Means

Necessary doesn’t mean essential or indispensable. The IRS defines it as “helpful and appropriate” for your business. That’s a lower bar than most people think. You don’t have to prove the conference was the only way to achieve a goal — just that attending it made sense for someone in your position running your type of business.

A real estate agent attending a local NAR conference? Clearly helpful and appropriate. That same agent attending a three-day culinary expo in New Orleans? You’d need a very good story.

The “Directly Related” Problem With Mixed-Purpose Conferences

This is where a lot of deductions fall apart. IRS Publication 463 draws a line between expenses that are directly related to your business and those that are merely associated with it. For most conference costs — registration, materials, sessions — direct relatedness is easy to establish. The trouble starts when personal elements creep in.

If your spouse joins you, if you extend the trip into a vacation, or if you attend sessions that have nothing to do with your business, the IRS will question whether the full cost qualifies. Partial deductions are fine. Pretending 100% of a mixed trip is business is not.

The “Helpful for Your Business” Documentation Test

In practice, the ordinary and necessary standard lives or dies by your documentation. The IRS isn’t going to audit every conference receipt — but if they do, they want to see:

- What the conference was (name, dates, location)

- Why it was relevant to your specific business

- Who attended (you, employees, clients)

- How much you paid, with receipts

One good method is keeping a brief written note — even a few sentences — in your records explaining the business purpose. Something like: “Attended SaaStr Annual 2024 to evaluate CRM vendors and meet with two existing software clients. Relevant to my B2B SaaS consulting practice.” That’s enough. It doesn’t need to be a legal brief.

When the Expense Fails the Test

Some conference costs simply don’t qualify, no matter how you categorize them. A few concrete examples:

- Tickets to the conference gala dinner that’s open to the public with no business agenda

- Sightseeing tours bundled into the registration package

- Personal hotel nights added before or after the business portion of the trip

- Registration for sessions that have no connection to your trade or profession

These don’t become deductible by putting them under “Professional Development” in Xero. The category label doesn’t create the deduction — the business purpose does.

Ordinary and Necessary Applies Per Expense, Not Per Trip

This is a point that catches people off guard. You can’t treat a conference trip as a single unit and declare it all deductible or all non-deductible. Each cost line gets evaluated separately. Your flight might pass the test. Your registration fee might pass. The scuba diving excursion packaged with the resort conference does not.

This is exactly why cost allocation matters — and why collapsing everything into one category is the wrong approach from both an accounting and a tax compliance standpoint.

The IRS Publication 535 definition of ordinary and necessary applies throughout all of this. It’s the same standard whether you’re filing on Schedule C as a self-employed person or submitting expense reports under an Accountable Plan as an employer. The category changes depending on context. The standard doesn’t.

How to Build a Company Conference Expense Policy

A clear written policy saves you from arguments at reimbursement time. Without one, employees guess — and they usually guess wrong. Registration fees end up in “Miscellaneous,” hotel costs go into “Office Expenses,” and suddenly your books are a mess that your accountant has to untangle at year-end.

Here’s how to build one that actually works.

What Every Conference Expense Policy Should Include

Start with the basics. Your policy should define which expense categories apply to conference costs — because, as covered throughout this guide, there isn’t just one.

At minimum, spell out:

- Which costs go into which category. Registration fees → Professional Development. Flights and hotels → Travel & Entertainment. Booth space → Marketing & Advertising. Meals → Meals (at 50% deductibility). Make this explicit so employees aren’t making judgment calls.

- Spending limits per category. Set a dollar cap on hotels (say, $250/night in standard markets, GSA per diem rates in high-cost cities), a meal per diem, and a registration fee threshold above which pre-approval is required.

- Who is eligible. Not every conference is appropriate for every role. Define whether attendance needs to be directly related to the employee’s current job function or whether future skill-building qualifies.

- Business purpose documentation. Every submission should include a written statement — even one sentence — explaining why the conference was a necessary business expense. This is straight out of IRS Publication 463, and it protects you if you’re ever audited.

- Mixed personal-trip rules. If an employee tacks a vacation onto a conference trip, your policy needs to state clearly how costs get split. Primary Purpose Test applies: if business is the main reason for the trip, transportation is fully deductible; if it’s not, none of it is. Hotel nights after the conference ends are personal. Write that down.

One more thing: if you reimburse employees under an Accountable Plan — which you should be — the policy itself is part of what makes that plan valid in the IRS’s eyes. An informal “just submit receipts and we’ll figure it out” approach doesn’t qualify.

Pre-Approval Process

Require approval before the money is spent. Not after. This is the piece most small companies skip, and it’s where the real problems start.

A practical pre-approval process looks like this:

- Employee submits a request that includes the conference name, dates, location, estimated total cost broken down by category, and a short business justification (two to three sentences is enough).

- Manager approves or denies within a set window — five business days is reasonable. They’re confirming the conference is relevant to the employee’s role and that the budget exists.

- Finance or accounting reviews anything above a threshold — say, $1,500 total. They check that costs are being categorized correctly before approval, not after the fact.

For virtual conferences, the process is simpler since there’s no travel involved, but you still want pre-approval for registration fees above a certain amount. A $49 webinar doesn’t need a paper trail. A $2,000 industry summit does.

Build the form in whatever tool you’re already using. QuickBooks has expense approval workflows. Xero has a similar feature. Even a simple Google Form feeding into a shared spreadsheet works for small teams. The tool matters less than the habit.

Receipt and Documentation Requirements

The IRS isn’t flexible on this. Under an Accountable Plan, employees must substantiate every expense with documentation that shows the amount, date, place, and business purpose. That’s not optional language — it’s the standard.

Here’s what you should require for each major conference cost type:

| Expense Type | Required Documentation |

|---|---|

| Registration/conference fees | Paid invoice or confirmation email showing amount and event name |

| Airfare | Itinerary plus receipt showing amount paid |

| Hotel | Itemized hotel folio, not just a credit card charge |

| Meals | Receipt plus names of attendees if it’s a business meal |

| Ground transportation | Receipts or rideshare app export |

| Booth or exhibitor fees | Contract and paid invoice |

Receipts over $75 are explicitly required per IRS Publication 463. But honestly, require receipts for everything above $25. It’s a cleaner rule and easier to enforce.

Set a submission deadline. Thirty days after the expense is incurred is standard. Employees who miss the window should have to explain why. If reimbursements happen outside the Accountable Plan’s timely return rules, they become taxable income to the employee — which nobody wants.

If your team travels frequently, expense apps like FreshBooks or a dedicated tool like Expensify let employees photograph receipts immediately and tag them to the right expense category on the spot. That dramatically reduces the end-of-trip “I lost the hotel folio” problem. Category errors get caught at entry, not three weeks later when someone is trying to close the books.

How to Enter Conference Expenses in Accounting Software — Step-by-Step

The category setup matters as much as the data entry. If your chart of accounts lumps everything into “Miscellaneous” or one giant “Travel” bucket, your reports are useless at tax time — and your accountant will charge you extra to sort it out.

Here’s how to handle it correctly in the three most common platforms.

QuickBooks (Online and Desktop)

Step 1: Set up the right expense accounts first.

Go to Accounting → Chart of Accounts → New. You want separate accounts for:

- Professional Development / Education & Training

- Travel (airfare, lodging, ground transport)

- Meals — Conference (50% deductible; keep it separate from fully deductible meals)

- Marketing & Advertising (for trade show booth fees, sponsorships)

- Dues & Subscriptions (if your conference fee includes a professional membership)

Don’t try to track meal deductibility inside a single travel account. QuickBooks has a built-in “Meals (50%)” account type — use it. That tag tells QuickBooks to apply the 50% limitation automatically when generating tax reports.

Step 2: Enter the conference registration fee.

Create an expense or bill. In the Category field, select “Professional Development” or “Education & Training.” In the Memo line, write the conference name, date, and business purpose. Thirty characters of description now saves a 30-minute phone call with your CPA in April.

Step 3: Split a single charge across multiple categories.

If you paid a hotel that bundled the room, parking, and a conference dinner on one invoice, use the Split feature on the transaction line. Allocate the room rate to Travel, the dinner to Meals (50%), and parking to Travel. Each line gets its own category. This is exactly where most small business owners make errors — they dump the total into Travel and call it done.

Step 4: Handle employee reimbursements.

If you’re reimbursing an employee under an Accountable Plan, create a Check or Bill Payment made out to the employee. Use the same expense categories as above. Do not run it through payroll unless the reimbursement is outside your Accountable Plan — in that case it becomes taxable wages, which is a different workflow entirely.

Step 5: Attach the receipts.

Use the receipt attachment icon on each transaction. IRS Publication 463 requires you to document amount, date, place, and business purpose. A photo of the receipt plus your memo line covers all four requirements.

Xero

Xero works on the same logic but the terminology differs slightly.

Go to Accounting → Chart of Accounts → Add Account. Set the account type to “Expense” and create the same breakdown: Professional Development, Travel, Meals & Entertainment, Marketing.

For conference expenses, use Accounts → Purchases → New Bill or submit through Expense Claims if it’s an employee out-of-pocket cost. On each line item, assign the correct account from your chart.

One Xero-specific note: the platform doesn’t automatically flag the 50% meals limitation the way QuickBooks does. You need to handle that adjustment manually, or via your tax software at year-end. Tell your bookkeeper explicitly — otherwise the deduction gets calculated wrong.

For split hotel bills, add multiple line items within the same bill. Same principle as QuickBooks.

FreshBooks

FreshBooks is simpler, which means less flexibility. It’s fine for sole proprietors and freelancers, but the chart of accounts customization is limited compared to QuickBooks or Xero.

Go to Expenses → Add an Expense. Choose or create a category. FreshBooks has default categories like “Travel” and “Professional Development” — use them as-is or rename them under Settings → Expense Categories.

The limitation: FreshBooks doesn’t natively handle the 50% meal limitation or cost allocation between business and personal trips. For a mixed-use conference trip, you’ll need to calculate the business-only percentage yourself (using the Primary Purpose Test day-count method) before entering the amounts. Enter only the deductible portion, and keep your allocation worksheet in your records as backup documentation.

General Rules Regardless of Platform

Use per diem rates where applicable. If your company reimburses employees using GSA per diem rates instead of actual receipts, code the per diem reimbursement to Travel or Meals based on the breakdown (the M&IE portion goes to Meals at 50%, lodging goes to Travel). Don’t just book the lump sum to one account.

Tag transactions consistently. Most platforms support tags or classes — use them to tag expenses by conference name or project. This makes it easy to pull a total cost report for any single event later.

Don’t create new accounts every time. A chart of accounts with 47 slightly different conference-related categories is just as bad as one. Standardize on five to seven expense accounts and use the memo/description field for specifics.

Reconcile before filing. Run your expense account detail reports and cross-check against your receipts before handing anything to your tax preparer. If the numbers on Schedule C or your corporate return don’t match your books, you have a problem — and finding it in February is better than finding it during an IRS correspondence audit in September.

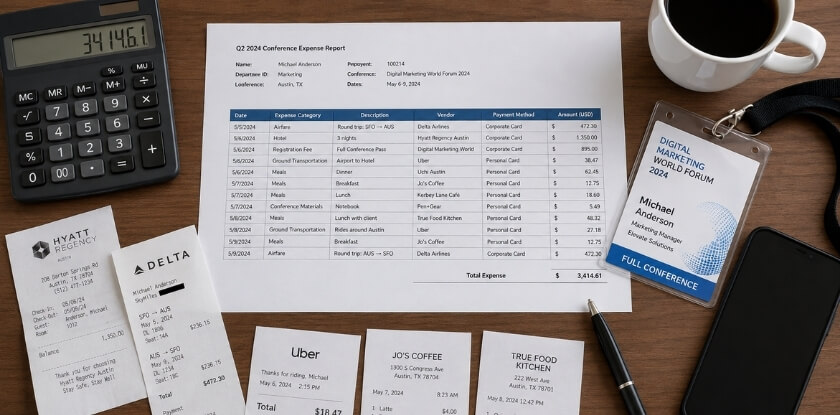

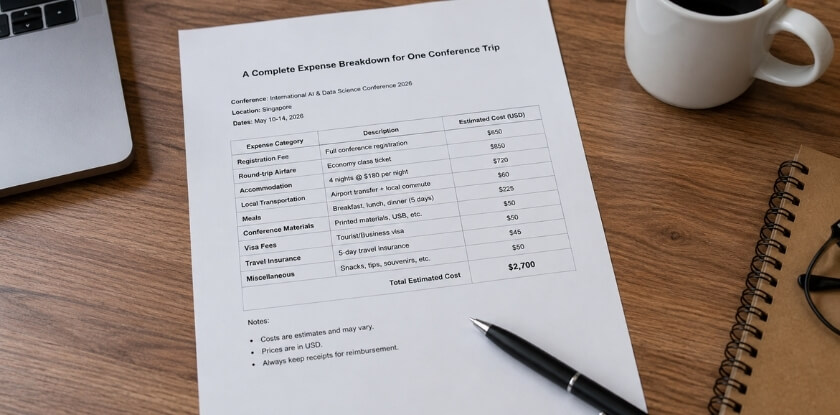

Real-World Example — A Complete Expense Breakdown for One Conference Trip

Let’s walk through a concrete scenario so all the categorization rules from earlier actually click into place.

The situation: Sarah is a self-employed marketing consultant who attends a three-day digital marketing conference in Chicago. She lives in Austin. She flies in a day early to meet a potential client for dinner, and she tacks on one extra day after the conference to visit her sister. Here’s every dollar she spent and exactly where it goes.

The Full Trip at a Glance

- Total trip: 5 days (1 pre-conference day, 3 conference days, 1 personal day)

- Business days: 4

- Personal days: 1

- Business-use percentage: 80%

Flight — $420 Round Trip

Category: Travel & Entertainment (T&E)

The primary purpose of the trip is business — four out of five days are business-related. That means the entire flight is deductible under IRS Publication 463 rules. Sarah doesn’t need to split the airfare 80/20. The whole $420 goes into her T&E travel bucket.

If the trip had flipped — more personal days than business — none of it would be deductible.

Conference Registration Fee — $895

Category: Professional Development / Education & Training

This is the cleanest line item on the whole trip. The registration fee goes directly to Education and Training, or Professional Development if that’s how her chart of accounts is set up in QuickBooks or Xero. It’s 100% deductible. No splitting required. She should keep the confirmation email and the conference agenda as documentation.

Hotel — $189/Night × 5 Nights = $945

Category: Travel & Entertainment (T&E) — Partially

This one needs a split. Four nights are business, one night is personal.

- Business portion: 4 × $189 = $756 → T&E / Lodging

- Personal portion: 1 × $189 = $189 → Not deductible

Sarah checks the GSA per diem rate for Chicago before filing. The GSA rate for lodging in Chicago runs around $179–$214 depending on the month, so her actual hotel cost is within a reasonable range and she’s using actual expense method rather than per diem. Both approaches are valid — she just has to pick one and stick with it.

Pre-Conference Client Dinner — $210 for Two

Category: Meals / Business Entertainment

This dinner happened the night before the conference with a legitimate prospective client. Post-TCJA, business meals are 50% deductible when there’s a genuine business discussion. Entertainment (like taking someone to a game) is no longer deductible at all.

- Deductible amount: $105

- Category in QuickBooks: Meals & Entertainment, with a note in the memo field: “Prospective client dinner — discussed potential retainer agreement”

That memo matters. The IRS wants to know who, what business purpose, and when.

Conference Meals (Per Diem Days) — 3 Days

Category: Meals / T&E

Sarah uses the GSA per diem meal rate for Chicago — let’s say $79/day for the conference days. She doesn’t save every receipt for every lunch; she uses the federal per diem rate instead.

- 3 days × $79 = $237

- 50% deductible = $118.50 → Meals & Entertainment

If she’d paid out of pocket and saved all receipts, she could deduct 50% of actual costs. Per diem is simpler for tracking purposes.

Workshop Add-On (Paid Separately) — $150

Category: Professional Development / Education & Training

This was a half-day copywriting workshop she registered for through the conference. Separate invoice, same category as the main registration fee. Goes in Education and Training. Fully deductible.

Uber/Lyft to and From Airport + Conference Venue — $74 Total

Category: Travel & Entertainment (T&E) — Transportation

All of it. Every ride during the business days is deductible. The one Uber she took to her sister’s place on the personal day? That $18 ride comes out of her own pocket and doesn’t go anywhere near her Schedule C.

Personal Day Costs — $0 Deductible

On her personal day, Sarah paid $55 for a museum ticket, $40 for dinner with her sister, and $22 for a rideshare. None of it is deductible. None of it gets entered into her accounting software as a business expense at all. Mixing those in, even accidentally, is exactly the kind of thing that creates problems during an audit.

Full Expense Summary Table

| Expense | Total Paid | Deductible Amount | Category |

|---|---|---|---|

| Airfare | $420.00 | $420.00 | T&E — Travel |

| Conference Registration | $895.00 | $895.00 | Professional Development |

| Hotel (4 business nights) | $756.00 | $756.00 | T&E — Lodging |

| Hotel (1 personal night) | $189.00 | $0 | Personal — Not deductible |

| Client Dinner (50%) | $210.00 | $105.00 | Meals & Entertainment |

| Conference Meals (per diem, 50%) | $237.00 | $118.50 | Meals & Entertainment |

| Workshop Add-On | $150.00 | $150.00 | Professional Development |

| Transportation (business days) | $74.00 | $74.00 | T&E — Transportation |

| Personal Day Expenses | $117.00 | $0 | Personal — Not deductible |

| Total | $3,048.00 | $2,518.50 |

What Sarah Does in Her Accounting Software

She creates a single expense report for the trip in QuickBooks, splits the hotel charge across two lines (business and personal), and attaches the PDF receipts to each entry. The conference registration and workshop invoices are tagged to her Education and Training category. All meal entries have memo notes with the business purpose.

Total deductible business expense from a $3,048 trip: $2,518.50.

The $529.50 that’s not deductible is real money. Knowing where the line sits keeps her audit-ready and her books clean.

Frequently Asked Questions (FAQ)

Is a conference registration fee tax-deductible?

Yes, in most cases. If the conference is directly related to your trade or business, the registration fee qualifies as an ordinary and necessary business expense under IRS rules. Sole proprietors deduct it on Schedule C. C-corps and S-corps deduct it as a business expense at the entity level. Employees who pay out of pocket can no longer deduct it federally — the Tax Cuts and Jobs Act eliminated unreimbursed employee expense deductions through 2025. Your state may still allow it, so check your state rules separately.

What expense category should I use in QuickBooks for a conference?

It depends on what the cost actually is. Registration fees go under Professional Development or Education and Training. Flights and hotels go under Travel. Meals at the conference go under Meals (at 50%). Booth rental or sponsored signage goes under Marketing and Advertising. QuickBooks lets you create sub-accounts, so you can track each type cleanly under its own parent category rather than dumping everything into one bucket.

Can I deduct 100% of conference meals?

No. Meals are capped at 50% deductibility under current IRS rules. That applies whether you’re eating alone between sessions or taking a client out to dinner after the keynote. The only exception would be meals that qualify as a de minimis fringe benefit for employees — those rare situations don’t come up often at conferences.

What if the conference is in a vacation destination like Las Vegas or Orlando?

The destination doesn’t change the rules. What matters is the Primary Purpose Test. If you spend more days on genuine conference business than on personal activities, you can deduct your transportation in full and your lodging and meals for the business days only. If you tack on three extra vacation days, you can’t deduct anything for those days. Keep your conference agenda, session attendance records, and hotel bills — the IRS looks for exactly this documentation when a conference is in a resort city.

How do I split expenses for a conference trip that was part business, part personal?

Day-by-day allocation. Count your total trip days, identify which were business days (travel days to and from the conference count), and calculate the ratio. Apply that ratio to shared costs like a rental car. Airfare is fully deductible if business days outnumber personal days — you don’t prorate flights. IRS Publication 463 covers the exact methodology.

Are virtual conference fees deductible the same way as in-person?

Yes. The IRS doesn’t distinguish between in-person and virtual for the underlying purpose test. A $500 virtual conference registration in your trade or profession is deductible the same way a $500 in-person registration is. The difference is that virtual conferences produce almost no travel or lodging costs, so the entire expense typically falls into one category — Professional Development — making categorization straightforward.

Does the 50% meal limit apply to conference-provided meals included in registration?

This is genuinely a gray area. If the meal is bundled into a registration fee you can’t itemize out, most accountants treat the whole fee as a professional development expense and don’t apply the 50% haircut to the meal portion, because you can’t separate it. If the conference separately bills a conference dinner or banquet, that’s a meal subject to the 50% limit. When in doubt, ask your accountant — the IRS hasn’t issued clear guidance on bundled meals.

What’s the difference between an Accountable Plan and just reimbursing employees for conference costs?

Under an Accountable Plan, employees submit receipts and documentation, and reimbursements aren’t reported as taxable income. Outside of that structure, reimbursements may need to be included in employee W-2 wages. For conference costs specifically, running reimbursements through a proper Accountable Plan keeps the expense deductible for the company and tax-free for the employee. It’s worth setting this up correctly before your next conference season, not after.

Can my company deduct a conference for a spouse who attended?

Only if the spouse is a bona fide employee with a genuine business reason to attend. “Moral support” or “networking” doesn’t cut it. If the spouse is on payroll and has a documented business role at the conference, the cost is defensible. If not, their costs — flights, hotel room upgrade, meals — are personal and non-deductible. This is a common audit flag.

Where do I find current per diem rates for conference travel?

The GSA publishes per diem rates by city at gsa.gov, updated annually each October. High-cost cities like San Francisco, New York, and Boston have higher lodging and M&IE rates than standard destinations. If you use the per diem method instead of tracking actual expenses, you use the rate for the city where the conference is held, not your home city. IRS Publication 463 explains how to apply these rates correctly.

Are trade show costs categorized differently than conference costs?

Often, yes. Attending a trade show as a visitor looks a lot like a conference — registration goes to Professional Development or T&E. But if you’re exhibiting, the cost structure changes. Booth rental, display materials, and branded giveaways belong in Marketing and Advertising. Staff travel to work the booth stays in Travel. Splitting these correctly matters, especially if you’re tracking marketing ROI separately from training spend.

What records do I actually need to keep?

At minimum: receipts for every expense, the conference agenda or program (showing its business relevance), dates of attendance, and the business purpose in writing. For meals, note who was present. For travel, keep your itinerary showing departure and return dates. Digital is fine — a folder in Google Drive or attached to your expense report in FreshBooks or Xero works. The IRS generally wants records that answer who, what, when, where, and why for each expense.